Non-Cash Gifts

Give Before Sale, Double the Tax Savings

Click on an item below for specific instructions on how to make a gift to your fund at the PCA Foundation, Inc.

Our church and the PCA Foundation provide general information and gift ideas for consideration by you and discussion with your own legal and other professional counsel, and not legal or other professional advice for your reliance. Neither our church, the PCA Foundation, nor any employee or other agent of either is permitted to or will provide legal or other professional advice or representation, and we urge you to seek legal and other professional counsel before making any significant gift.

Why Non-Cash Gifts

Let’s consider first why you would give non-cash assets – or employ any other tax-efficient giving strategy.

It’s not to make yourself wealthier post-gift because no charitable giving can ever leave the giver with greater wealth, no matter how much tax it saves. Nor is it to give wealth to charity instead of the government because tax savings can only ever be a percentage less than 100 of the amount given. To illustrate simply, the giver with a marginal tax rate of 35% who gives $1,000 to charity and deducts $1,000 from his taxable income effectively saves only $350 in tax. So, after the gift, and after the tax rebate, he still is $650 poorer than before he made the gift.

No, the reason to make the gift that saves the most in taxes is to be able to give MORE. In our simple example, the $350 tax savings produced by the charitable deduction mean that the $1,000 gift effectively cost our giver only $650. As every amateur economist knows, when something costs less, one can buy more of it. Here, the giver can give more – at least $350 more. Calculated more precisely, the giver can give the amount of wealth with which he is willing to part, $1,000, divided by 1 minus the tax rate, 65%: he can give $1,538 ($1,000/.65), or $538 more.

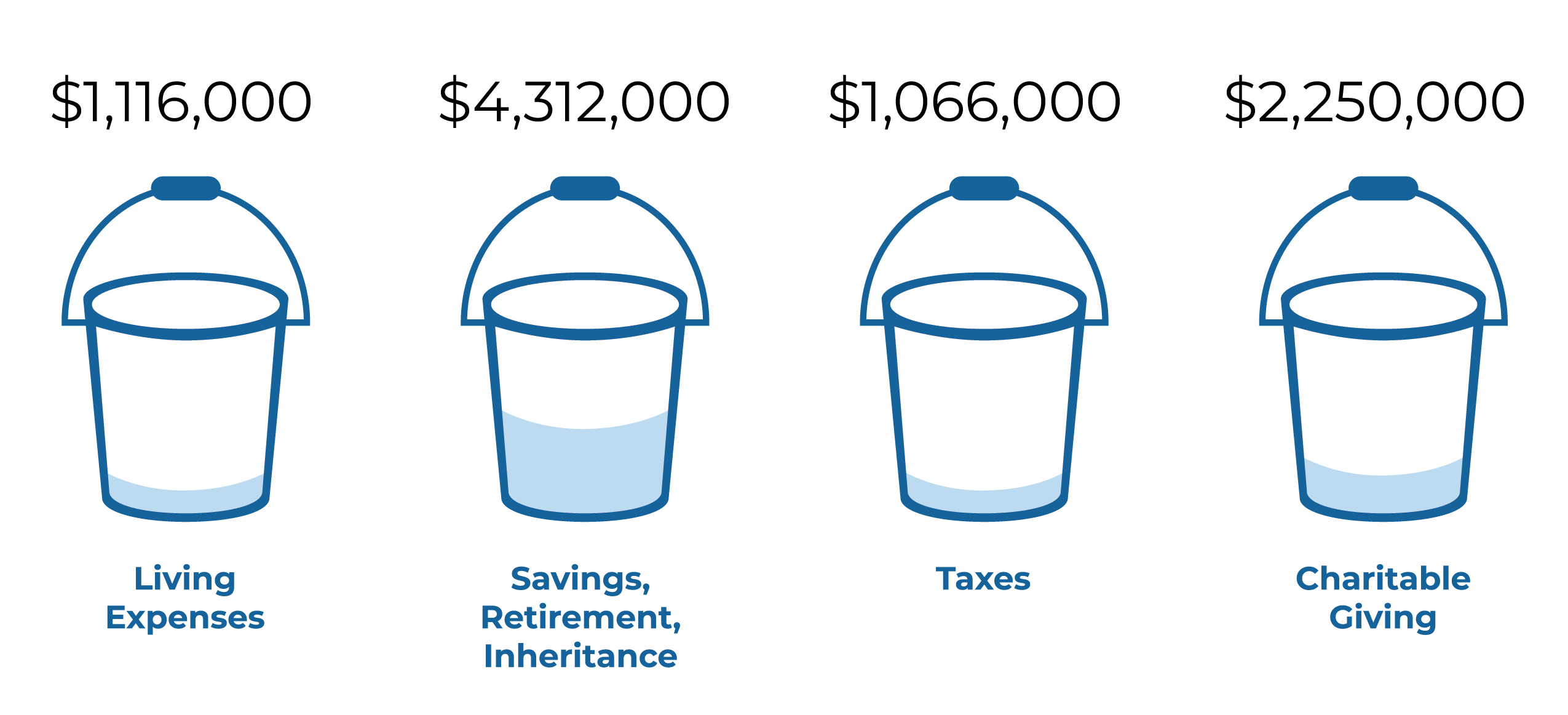

Or envision four “buckets” into which you can place your income and wealth:

Whenever you decide how much to place in the giving bucket as cash, you actually are deciding in your Spirit-changed heart how much to keep in the consumption and savings buckets. You then employ non-cash giving to move greater tax savings from the tax bucket to the giving bucket, while leaving the same amounts in the consumption and savings buckets.

In a word, give non-cash assets and you can give more to your church and other charities.

Stocks and Bonds

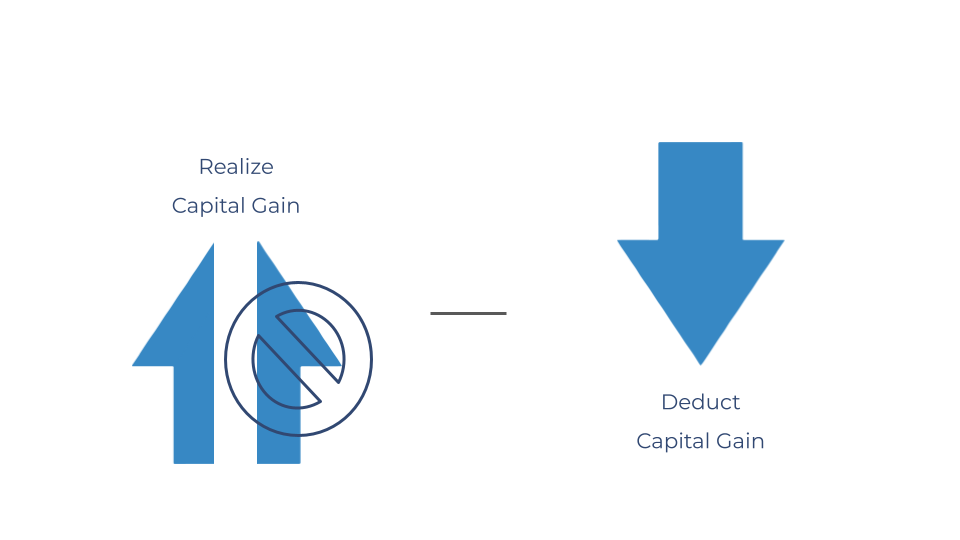

Donating appreciated publicly-traded stock, mutual funds, or bonds instead of cash allows you to avoid the capital gains tax you otherwise would incur on sale while receiving a charitable deduction for the full market value. You effectively realize a double deduction of the appreciation that reduces taxes and thereby enables you to give more. Once the PCA Foundation sells the stock or other securities you give to it, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.

STOCK AND BOND GIVING

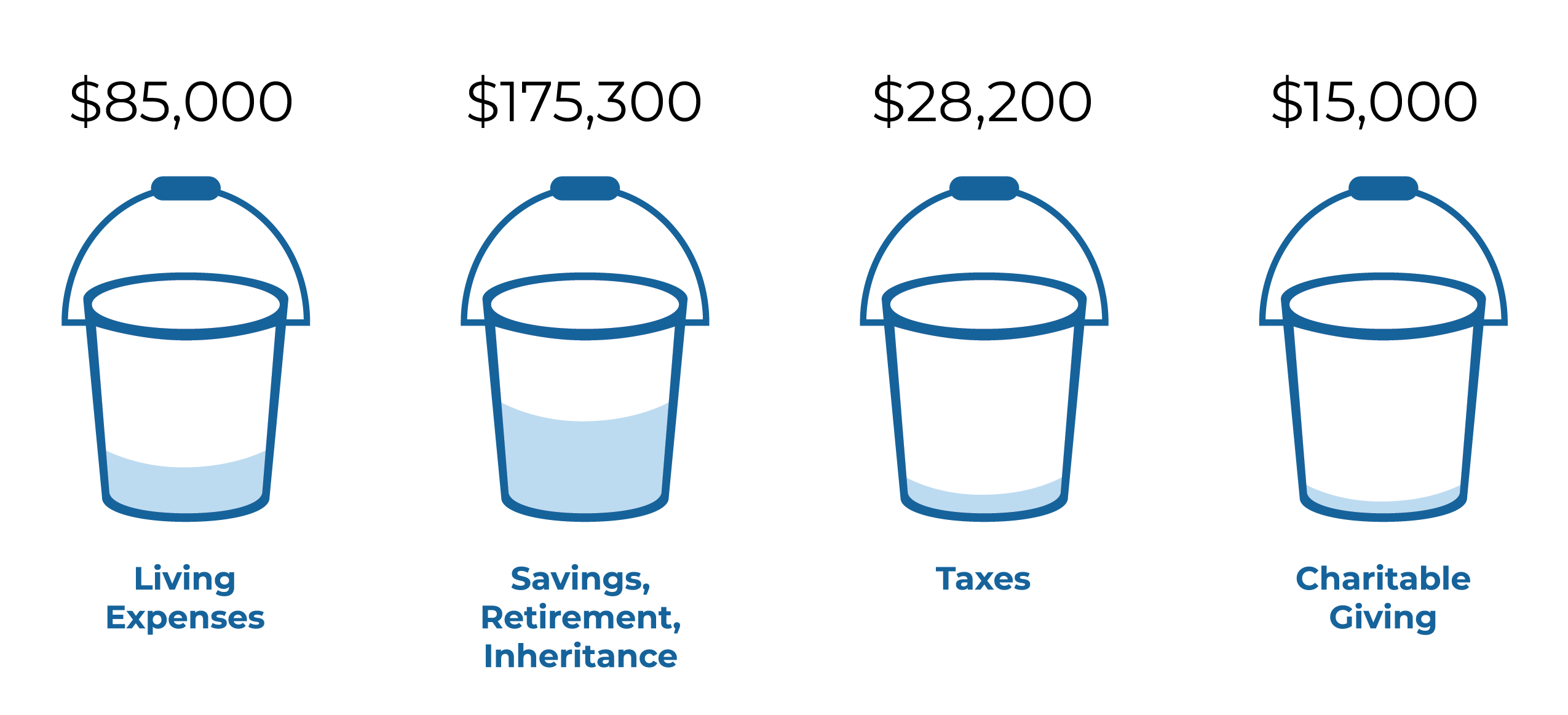

Here’s an example: the Johnsons are a couple with compensation and other ordinary taxable income for the year of $150,000. They expend $85,000, and want to tithe $15,000. They have a relatively small investment portfolio of $150,000, of which $50,000 is publicly-traded stock that is appreciated 35%. Here are possible year-end results of giving their 10% tithe as cash, assuming certain additional financial circumstances and treating the capital gains tax to be paid eventually on a sale of the appreciated stock as a lien against that stock that effectively reduces its value:

THE JOHNSONS GIVE CASH

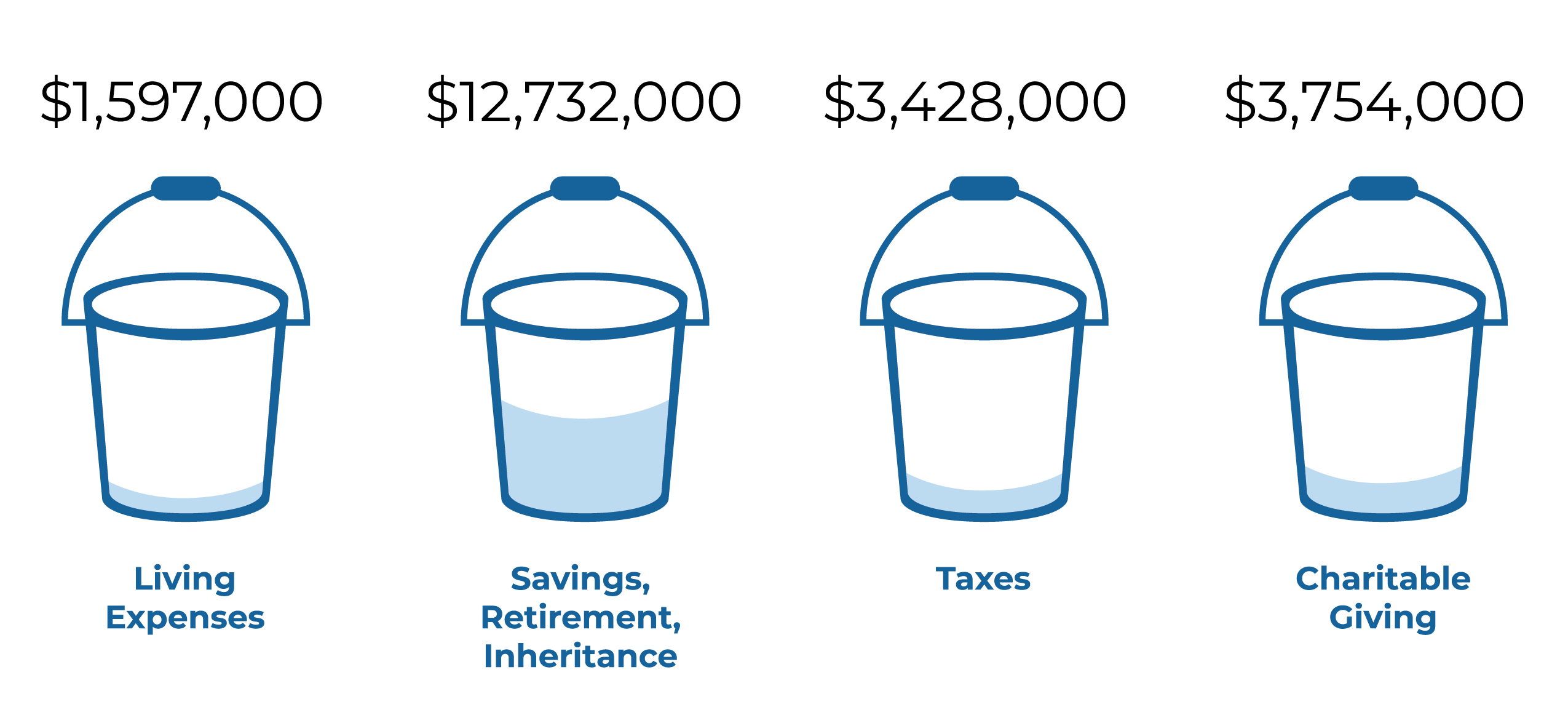

And here are possible results at the end of the year under the same financial assumptions of instead giving a portion of their 35%-appreciated cryptocurrency instead:

THE JOHNSONS GIVE STOCK

The Johnsons exclude the 35% appreciation from taxable capital gain, and so reduce their federal and state tax to $26,900. They save $1,300 in tax and give away $1,300 more while keeping the same $85,000 for personal expenditures and putting away the same $175,300 in savings.

Even if you do not plan to sell your stock, mutual fund, or bond currently, you still can achieve the double deduction by giving the security now and then buying the same security with the cash you otherwise would have given. When you do, you effectively increase your basis in the security and thereby permanently eliminate the built-up capital gain and the looming tax on that gain.

To make a gift, visit the PCA Foundation’s gifting instructions page and click on the appropriate category: for gifts via broker transfer, or gifts via transfer of stock certificates.

Real Estate Gifts

You may make a charitable gift of all or only part of an undivided interest in developed or undeveloped real estate. Undivided real estate interests you can give include mineral (including oil and gas) estates and overriding royalty interests although giving working mineral interests can be problematic – consult with the Foundation about your particular interest. (“Undivided interest” means all or a percentage of the entire bundle of rights that you own with regard to the real estate. For example, you may give a 100% fee simple interest, or a 20% tenancy in common, but you may not split off and give a leasehold interest in the property while retaining the fee – unless that leasehold interest is all you own, or separate the surface estate from the mineral estate in a parcel of real estate and give only one or the other – again, unless the estates were previously separated and you own only one of them, the surface or the mineral.)

When you give appreciated real estate you exclude from your taxable income the capital gain you otherwise would realize if you sell (the equivalent of a deduction), and you also actually deduct the full market value of the real estate. You effectively realize a double deduction of the appreciation that reduces your income taxes and enables you to give significantly more. As the Foundation receives income from the real estate you give to it, and then sells the real estate, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.

REAL ESTATE GIVING

Here’s an example: Mr. Baker is a real estate developer. The Bakers are 60 years old and have:

an investment portfolio of $1,000,000,

developed unencumbered commercial real estate worth $5,000,000, with a basis of $1,000,000, and

annual taxable income of $500,000, of which they give away 15%.

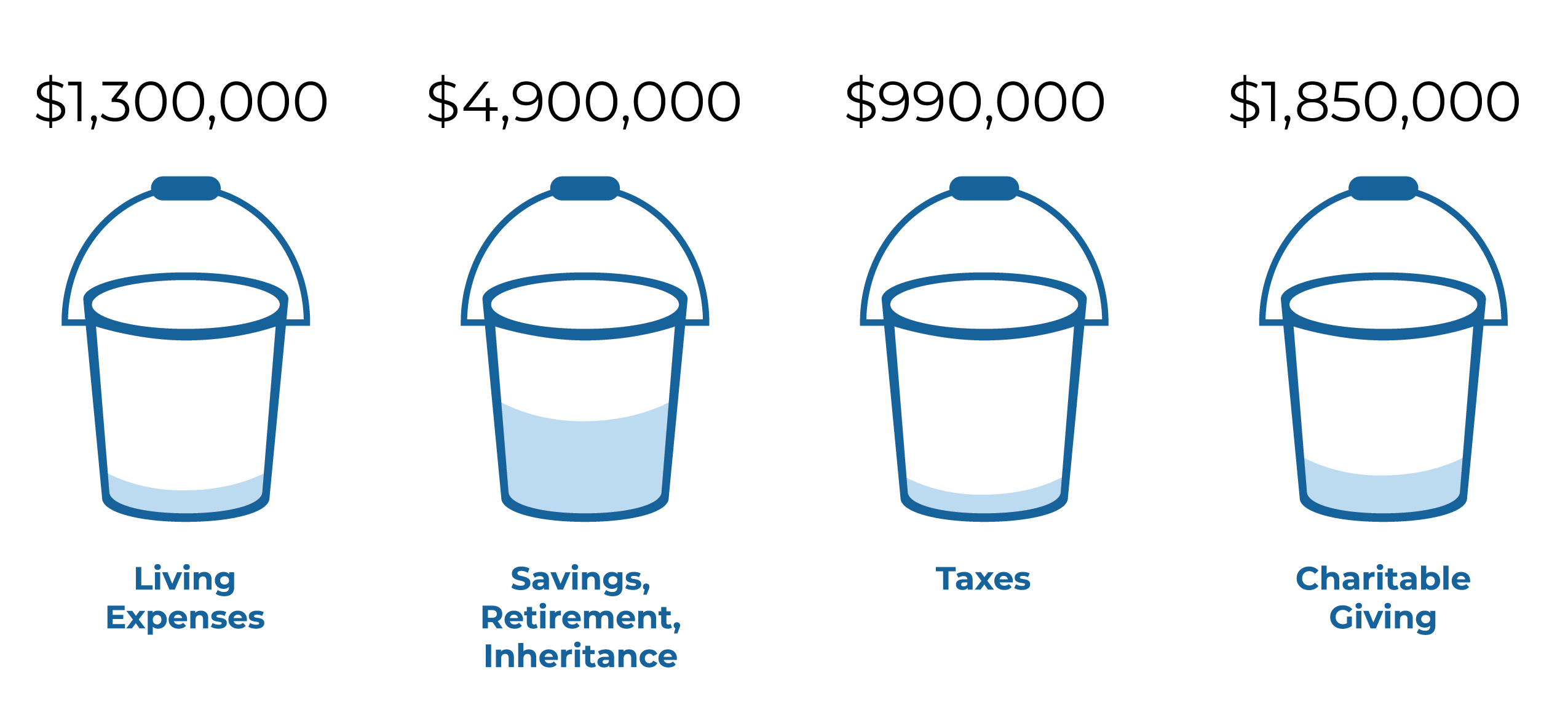

The Bakers intend to sell their real estate holding, and the love of Christ arising from their confession of the Gospel prompts them to give from the cash sale proceeds 30% of the capital gain, or $1,200,000. Here are possible results of their cash giving at the end of six years (the current year plus 5 years to which it may be necessary to carry forward excess deductions) assuming certain additional financial circumstances:

And here are possible results at the end of the same period and under the same financial assumptions of instead giving an interest in the real estate before sale:

The Bakers exclude from their taxable income the capital gain in the portion of the real estate they give while also deducting from other taxable income and gain the full fair market value of the real estate, thereby saving taxes that they also give and deduct. And the greater gift amount placed in their donor-advised fund grows tax-free over the period. They are able to give $460,000, or 25%, more while keeping the same amounts for spending and savings.

As with all non-cash gifts, it is important to remember that if you enter into a binding sales contract before you donate the property, the IRS will treat your gift of real estate followed by a sale as a taxable sale of the real estate followed by a gift of the cash proceeds (denying the effective double deduction). Consult with the PCA Foundation if you are about to enter or think you may have entered an agreement to sell or letter of intent that may be a binding agreement to sell. In general it is important to have your initial conversation with the PCA Foundation as early as possible if you are considering a real estate gift. Their experts will help you navigate the complexities of the real estate donation to increase your giving potential.

Speaking with the PCA Foundation is even more crucial if the real estate is encumbered by debt, as substantial debt can result in the Foundation paying much of the tax that the giver avoided, thereby reducing the amount available for ultimate giving. Worse, encumbrance by debt can result in the giver incurring income tax on the gift. It frequently is advantageous to pay off or transfer to other property all debt encumbering real estate before donating it, but other circumstances and strategies may mitigate the effects of debt as well. Please consult with the Foundation.

Be aware also that if the sale of the real estate would have resulted in recapture ordinary income instead of capital gain, your charitable deduction upon gifting will be reduced by the amount of such income. Such recapture income might occur, for example, if you have taken accelerated depreciation deductions for the real estate. The reduced deduction might or might not make the benefits of giving the property rather than cash not worth the extra effort. Again, you will want to consult with the Foundation.

Partnership Interest Gifts

You may make a charitable gift of all or only part of an undivided interest in a business entity organized as a partnership. Partnership interests you can give include units in a limited liability company that has elected to be taxed as a partnership (“LLC”), and limited partnership interests in a limited partnership (“LP”). Giving general partnership interests can be problematic – consult with the Foundation. (“Undivided interest” means all or a percentage of the entire bundle of rights you own with regard to the partnership. For example, you can give 20% of the ownership interests in the partnership, but you cannot give only the profits interest in the partnership – unless that is the only interest you own.)

When you give appreciated partnership units you exclude from your taxable income the capital gain you otherwise would realize if you sell (the equivalent of a deduction), and you also actually deduct the full market value of the units. You effectively realize a double deduction of the appreciation that reduces your income taxes and enables you to give more. As the Foundation receives income from the partnership units you give to it, and then when it sells the partnership units, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.

PARTNERSHIP GIVING

Here’s an example: The Kims are a 55-year-old couple with:

an investment portfolio of $800,000,

units in an import business organized as a LLC and taxed as a partnership, worth $5,000,000, with a basis of only $100,000, and

annual taxable ordinary income of $283,000, consisting of employment compensation, partnership pass-through income, and dividends and interest from brokerage accounts, of which ordinary income they give away 15% to our church.

The Kims are approaching a sale of their import business, and Christ’s love in the Gospel prompts the Kims to give thirty percent of the accumulated capital gain in the business, or $1,470,000, to our church and other charities over several years. Here are possible results of their cash giving at the end of six years (the current year plus 5 years to which it may be necessary to carry forward excess deductions) assuming certain additional financial circumstances:

And here are possible results at the end of the same period and under the same financial assumptions of instead giving a number of their LLC units before sale:

Personal expenditure remains the same; ending savings remain the same; but taxes go down significantly, by $461,000, due to exclusion of capital gains tax on the gifted units (the equivalent of a deduction), and the actual deduction for their full market value – effectively, a double deduction. Put another way, due to the tax savings/rebate, every dollar of units given costs the Kims less than does a dollar of cash given – perhaps only 55 cents instead of 75 cents. Plus, the greater amount placed in their donor-advised fund grows tax free over the period. So, the Kims are able to give more dollars, $892,000 more, to our church and the other ministries they support.

As with all non-cash gifts, it is important to remember that if you enter into a binding sales contract before you donate your privately-held partnership units, the IRS will treat your gift of units followed by a sale as a taxable sale of the units followed by a gift of the cash proceeds (denying the effective double deduction). Consult with the PCA Foundation if you are about to enter or think you or the partnership may have entered an agreement or letter of intent that may be a binding agreement to sell your units or the partnership’s assets. In general it is important to have your initial conversation with the PCA Foundation as early as possible if you are considering a gift of privately-held partnership units. Their experts will help you navigate the complexities of the unit donation to increase your giving potential.

Be aware of a couple circumstances that may reduce, or in some cases nearly eliminate the double-deduction benefit of giving partnership units instead of cash. First, if your units or the partnership’s assets are encumbered by substantial debt, the Foundation will be required to pay, as debt-financed unrelated business income tax (UBIT), much of the tax that you avoid, thereby reducing the amount available for ultimate giving. Worse, encumbrance by debt can result in you actually incurring income tax on the gift itself. It frequently is advantageous to pay off or transfer to other property all debt encumbering stock before donating it, but other circumstances and strategies may mitigate the effects of debt as well. Please consult with the Foundation.

Second, if your partnership has certain kinds of assets – called “hot assets” – the sale of which would result in recapture ordinary income instead of capital gain, your charitable deduction upon gifting will be reduced by the amount of such income. Examples of hot assets include inventories, unrealized receivables, and property for which the partnership has taken accelerated depreciation deductions. The reduced deduction might or might not make the benefits of giving the units rather than cash not worth the extra effort. Again, you will want to consult with the Foundation.

If your partnership is engaged in an active business, it’s important to know that a donor-advised fund typically must liquidate within five years of the gift the partnership units given that are more than 20% of the total ownership interest reduced by the percentage of units held by you and related persons. If, for example, you own 35% of the partnership units, then give the Foundation 20%, the Foundation must dispose of 15% within 5 years of the gift. Typically, the Foundation plans to sell partnership units it receives well before the expiration of 5 years from the date of gift. However, speak with the Foundation about circumstances and the various strategies it has developed to facilitate holding ownership interests for longer periods in order to grant just the income they produce.

C Corporation Gifts

In addition to gifts of publicly-traded C Corporation stock (see Stock and Bond Gifts), you may make a charitable gift of all or only part of an undivided interest in privately-held C Corporation stock. (“Undivided interest” means that you may not give common stock but retain its voting rights, for example.) When you give appreciated C Corporation stock you exclude from your taxable income the capital gain you otherwise would realize if you sell (the equivalent of a deduction), and you also actually deduct the full market value of the stock. You effectively realize a double deduction of the appreciation that reduces your income taxes and enables you to give more.

As the Foundation receives distributions on the stock you give to it, and then when it sells the stock, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to multiple ministries over time.

C CORPORATION GIVING

Here’s an example: The Bryants are 50 years old and have:

an investment portfolio of $800,000,

privately-held common stock in a C business corporation worth $500,000, with a basis of $100,000, and

annual taxable ordinary income of $270,000, consisting of employment compensation and dividends on the stock, of which ordinary income they give away 10% to our church.

A buyer has approached the Bryants and their co-shareholders to sell their stock in the company, and they have determined in their-Spirit-changed hearts to give from the cash sale proceeds 30% of the capital gain, or $120,000. Here are possible results of their cash giving at the end of two years (the current year plus an additional year to which it may be necessary to carry forward excess deductions) assuming certain additional financial circumstances:

And here are possible results at the end of the same period and under the same other financial assumptions of instead giving an interest in the C Corporation before sale:

The Bryants exclude from their taxable income the capital gain in the C Corporation stock they give while also deducting from other taxable income and gain the full fair market value of the stock, thereby saving taxes that they also give and deduct. And the greater gift amount placed in their donor-advised fund grows tax-free over the period. They are able to give $57,000, or 31%, more while keeping the same amounts for spending and savings.

As with all non-cash gifts, it is important to remember that the IRS will treat your gift of privately-held C Corporation stock followed by a sale as a taxable sale of the stock followed by a gift of the cash proceeds (denying the effective double deduction) if you enter into a binding sales contract before you donate the stock. Consult with the PCA Foundation if you are about to enter or think you or the company may have entered an agreement or letter of intent that may be a binding agreement to sell. In general it is important to have your initial conversation with the PCA Foundation as early as possible if you are considering a gift of privately-held stock. Their experts will help you navigate the complexities of the stock donation to increase your giving potential.

While not common, if the stock is encumbered by substantial debt, the Foundation will be required to pay, as debt-financed unrelated business income tax (UBIT), much of the tax that the giver avoids, thereby reducing the amount available for ultimate giving. Worse, encumbrance by debt can result in the giver actually incurring income tax on the gift. It frequently is advantageous to pay off or transfer to other property all debt encumbering stock before donating it.

If your C Corporation is engaged in an active business, it’s important to know that a donor-advised fund typically must liquidate within five years of the gift the stock given that is more than 20% of the total ownership interest reduced by the percentage of shares held by you and related persons. If, for example, you own 35% of the stock, then give the Foundation 20%, the Foundation must dispose of 15% within 5 years of the gift. Typically, the Foundation plans to sell stock it receives well before the expiration of 5 years from the date of gift. However, speak with the Foundation about circumstances and the various strategies it has developed that facilitate holding business ownership interests for longer periods in order to grant just the income they produce.

S Corporation Gifts

You may make a charitable gift of all or only part of an undivided interest in a business entity organized in the most common form of small to medium-sized businesses, the pass-through S Corporation. (“Undivided interest” means all or a percentage of the entire bundle of rights you own with regard to the S Corporation. For example, you can give 20% of the stock in the S Corporation, but you cannot give the stock and retain its voting rights – but you can give nonvoting stock if that is what you own.)

When you give appreciated S Corporation stock you exclude from your taxable income the capital gain you otherwise would realize if you sell (the equivalent of a deduction), and you also actually deduct the full market value of the stock. However, a special rule in the tax code requires that when the Foundation is allocated income from S Corporation stock it receives, or realizes gain when it sells the stock, it must recognize the taxable income or gain that you avoided, as unrelated business taxable income (“UBTI”). But the Foundation is organized as a trust and therefore is allowed to deduct against that UBTI, up to half of it, the grants it makes each year (as its own deductible charitable contributions). So, instead of the effective double deduction you realize when you give units of another type of pass-through entity, the partnership (see Partnership Interest Gifts), you effectively realize a one and one-half times deduction of the appreciation in the stock. This reduces income taxes for you and the Foundation and enables you ultimately to give more.

As the Foundation receives income distributions on the stock you give to it, and then when it sells the stock, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.

S CORPORATION GIVING

Here’s an example: The Bells are 55-year-old tech entrepreneurs with three children and with:

an investment portfolio of $1,500,000,

one-third of the stock in a technology business organized as an S Corporation, worth $12,000,000, with a basis of only $500,000, and

annual taxable ordinary income of $897,000, consisting of employment compensation, S Corporation pass-through income, and dividends and interest from brokerage accounts, of which ordinary income they give away 10% to our church and other charities.

A venture capital firm has approached the Bells and their co-owners to buy the technology business they founded. The love of Christ formed in the Bells’ hearts to date leads them in consideration of all their circumstances, including plans to start another business, to give twenty percent of the accumulated gain in their stock, or $2,300,000, to their church and other charities over several years beginning five years from now. Here are possible results of their cash giving at the end of six years (the current year plus 5 years to which it may be necessary to carry forward excess deductions) assuming certain additional financial circumstances:

And here are possible results at the end of the same period and under the same financial assumptions of instead giving a number of their stock shares before sale:

Personal expenditure remains the same; ending savings remain the same; but taxes go down significantly, by $1,076,000, due to exclusion of one-half the capital gains tax on the gifted stock (the equivalent of a deduction), and the actual deduction for their full market value – effectively, a one and one-half times deduction. Put another way, due to the tax savings/rebate, every dollar of stock given costs the Bells less than does a dollar of cash given – perhaps only 50 cents instead of 70 cents. Plus, the greater amount placed in their donor-advised fund grows tax free over the period. So, the Bells are able to give more dollars, $1,821,000 more, to our church and the other charities they support.

As with all non-cash gifts, it is important to remember that if you enter into a binding sales contract before you donate your S Corporation stock, the IRS will treat your gift of stock followed by a sale as a taxable sale of the stock followed by a gift of the cash proceeds (denying the effective one and one-half times deduction). Consult with the PCA Foundation if you are about to enter or think you or the S Corporation may have entered an agreement or letter of intent that may be a binding agreement to sell your stock or the corporation’s assets. In general it is important to have your initial conversation with the PCA Foundation as early as possible if you are considering a gift of S Corporation stock. Their experts will help you navigate the complexities of the stock donation to increase your giving potential.

Be aware that if your S Corporation has certain kinds of assets – called “hot assets” – the sale of which would result in recapture ordinary income instead of capital gain, your charitable deduction upon gifting will be reduced by the amount of such income. Examples of hot assets include inventories, unrealized receivables, and property for which the corporation has taken accelerated depreciation deductions. The reduced deduction might or might not make the benefits of giving the stock rather than cash not worth the extra effort. You will want to consult with the Foundation.

If your S Corporation is engaged in an active business, it’s important to know that a donor-advised fund typically must liquidate within five years of the gift the stock given that is more than 20% of the total stock of the corporation reduced by the percentage of stock held by you and related persons. If, for example, you own 35% of the stock, then give the Foundation 20%, the Foundation must dispose of 15% within 5 years of the gift. Typically, the Foundation plans to sell stock it receives well before the expiration of 5 years from the date of gift. However, speak with the Foundation about circumstances and the various strategies it has developed to facilitate holding stock for longer periods in order to grant just the income it produces.

Cryptocurrency Gifts

The opinions of cryptocurrency as an investment vary widely. Our church and the PCA Foundation do not invest in cryptocurrency, and of course do not advise any person about their investment choices. However, if you do own appreciated cryptocurrency, it makes a highly effective charitable gift.

Donating appreciated cryptocurrency allows you to avoid the capital gains tax you otherwise would incur on sale while receiving a charitable deduction for the full market value. You effectively realize a double deduction of the appreciation that reduces taxes and thereby enables you to give more.

Once the Foundation sells the cryptocurrency you give, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.

CRYPTOCURRENCY GIVING

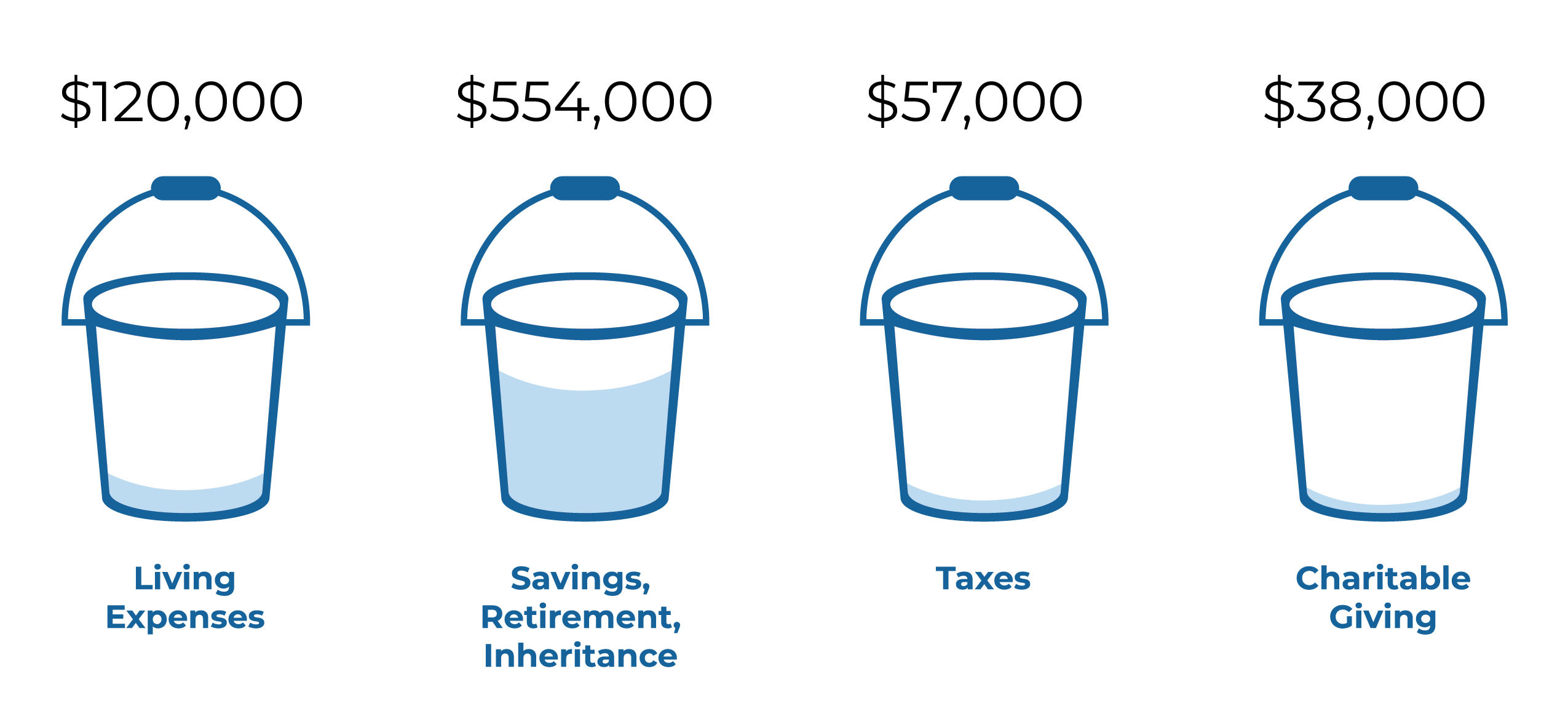

Here’s an example: the Haileys are a couple with compensation and other ordinary taxable income for the year of $253,000. They expend $120,000, and want to tithe 15%, or $37,950. They have a typical investment portfolio of $300,000, but they also own cryptocurrency that they purchased for $20,000 and that has appreciated to a market value of $200,000. Here are possible year-end results of giving their 15% tithe as cash, assuming certain additional financial circumstances and treating the capital gains tax to be paid eventually on a sale of the cryptocurrency as a lien against that crypto that effectively reduces its value:

And here are possible results at the end of the year under the same financial assumptions of instead giving a portion of their 90%-appreciated cryptocurrency instead:

The Haileys exclude the 90% appreciation on the cryptocurrency from taxable capital gain, and so reduce their current and eventual federal and state tax to $30,000. They save $27,000 in tax and give away $27,000 more while keeping the same $120,000 for personal expenditures and effectively putting away the same $554,000 in savings.

Even if you do not plan to sell your cryptocurrency currently, you still can achieve the double deduction by giving the crypto now and then buying the same amount of crypto back with the cash you otherwise would have given. When you do, you effectively increase your basis in the crypto and thereby permanently eliminate the built-up capital gain and the looming tax on that gain.

To make a gift, visit the PCA Foundation’s gifting instructions page and click on the cryptocurrency category.

Stock Options

While you can give neither incentive stock options nor nonstatutory stock options while living, having incentive stock options creates a great opportunity to save taxes and give more. You cannot transfer an incentive stock option prior to death, but once you have received the necessarily appreciated stock upon exercise of the option, and held it for the required holding period, you can give the stock. When you do, you avoid the capital gains tax you otherwise would incur on a sale of the stock while receiving a charitable deduction for its full market value. You effectively realize a double deduction of the inherent appreciation in the stock at the exercise of the option and any appreciation since exercise. You reduce taxes accordingly, thereby enabling you to give more.

OPTION STOCK GIVING

See the sections of this website on public stock, C Corporation Gifts and S Corporations for further explanation of the benefits of giving appreciated stock, relevant considerations, and illustrations, or to make or propose a gift.

Note that in contrast to gifts of stock received upon exercise of incentive stock options, gifts of stock received upon exercise of nonstatutory stock options are no more tax-efficient – and may be less – than gifts of cash. Note also that you may bequeath to charity both qualified incentive stock options and nonstatutory stock options, and such options are better given to charity than to taxable heirs. (See Charitable Bequests)

Once the Foundation sells the appreciated stock received upon exercise of an incentive stock option, it places the proceeds in a fund established for our church, or into your own donor-advised fund (see Donor Advised Funds) from which you can grant the proceeds just to our church or to church and multiple other charities over time.