Estate Giving

Plan giving for the rest of life, and beyond

Click on an item below for specific instructions on how to make a gift.

Our church and the PCA Foundation provide general information and gift ideas for consideration by you and discussion with your own legal and other professional counsel, and not legal or other professional advice for your reliance. Neither our church, the PCA Foundation, nor any employee or other agent of either is permitted to or will provide legal or other professional advice or representation, and we urge you to seek legal and other professional counsel before making any significant gift.

Charitable Bequests

One of the easiest gifts to make is simply to remember our church in your will, living trust, or retirement account. Instruct your legal counsel to draft a bequest in your will or charitable distribution in your living trust to “Example Church , 123 Demo Street, City, State 12345 .” This simple step can provide for our work in the Gospel for years to come. If you have specific projects that you would like to fund, please talk with us so we can plan with you and ensure that we understand your vision for your gift.

If you desire to benefit additional organizations at end of life, or want to be able during life to change charitable beneficiaries without the additional cost and burden of amending your will or trust, we recommend opening a donor advised fund (DAF) (see Donor Advised Funds) at the PCA Foundation and naming it as the sole charitable beneficiary. Then, simply file instructions with the Foundation for ultimate granting to our church and other charities after your death, and amend those instructions as your charitable objects change over the course of your life. You can learn more about the usefulness of DAFs in estate planning here.

As you decide what assets to bequeath to children and other taxable heirs, and what to bequeath to charity, consider this simple rule: to the extent possible, bequeath to children and other taxable heirs appreciated assets, and bequeath to charity retirement accounts, commercial annuities, and qualified incentive stock options and nonstatutory stock options (see Stock Options]). Taxable heirs receive a step-up in basis of appreciated assets, and therefore do not pay capital gains tax on built-up appreciation when they sell the assets, but they pay tax on the income in respect of a decedent that you would have earned upon distribution of retirement amounts, annuity payments, and sale of optioned stock. A tax-exempt charity, meanwhile, does not pay tax on such income in respect of a decedent.

We recognize that general estate planning – for provision for both heirs and church and charity – can seem overwhelming. Thankfully, the PCA Foundation has provided this free resource to help you begin planning. Once you have completed the worksheets, you can meet with your attorney for counsel and to have the necessary paperwork prepared. If you do not have an estate-planning attorney, we or the Foundation would be happy to help you find one.

Why Accelerate Giving

Before moving on to consider ways of bringing forward while you are living the charitable giving you anticipate at end of life (Charitable Bequests), let’s consider why you would so accelerate your giving. The first answer, of course, is that you do not receive a charitable income tax deduction for charitable bequests, and thus do not save taxes. But why would you want to save taxes by accelerating giving – or employing any other tax-efficient giving strategy?

It’s not to make your heirs wealthier post-gift because no charitable giving can ever leave the giver or his heirs with greater wealth, no matter how much tax it saves. Nor is it to give wealth to charity instead of the government because tax savings can only ever be a percentage less than 100 of the amount given. To illustrate simply, the giver with a marginal tax rate of 35% who gives $1,000 to charity and deducts $1,000 from his taxable income effectively saves only $350 in tax. So, after the gift, and after the tax rebate, he and ultimately his heirs still are $650 poorer than before he made the gift.

No, the reason to make the gift that saves the most in taxes is to be able to give MORE. In our simple example, the $350 tax savings produced by the charitable deduction mean that the $1,000 gift effectively cost our giver and his heirs only $650. As every amateur economist knows, when something costs less, one can buy more of it. Here, the giver can give more – at least $350 more. Calculated more precisely, the giver can give the amount of wealth with which he is willing to part, $1,000, divided by 1 minus the tax rate, 65%: he can give $1,538 ($1,000/.65), or $538 more.

Or envision four “buckets” into which you can place your income and wealth:

Whenever you decide how much to place in the giving bucket as cash, you actually are deciding in your Spirit-changed heart how much to keep in the consumption and inheritance buckets. You then accelerate giving to move greater tax savings from the tax bucket to the giving bucket, while leaving the same amounts in the consumption and inheritance buckets.

In a word, accelerate giving to taxable-income years and you can effectively bequeath more to your church and other charities while bequeathing the same to your children and other heirs.

Accelerated Giving

Give during High Earning Years, Reduce Taxes, Enable Greater Giving

When you make an end of life donation, you lose one powerful tool for giving: a tax deduction. Charitable contributions made by bequest at death are not deductible, and therefore do not produce the tax savings – the tax subsidy – that would reduce the cost of giving and thereby enable more of it.

But charitable contributions made during years of taxable income are deductible, and do produce those tax savings and that tax subsidy. So, to achieve those tax savings for greater giving, project how much you desire to leave to taxable heirs, leaving the rest to charity. Then determine for each year the amount of wealth that will grow just to the inheritance you desire to pass at death – this is the glide path to the inheritable estate. Then determine for each remaining year of taxable income the lesser of the amount that will bring your personal wealth down to the glide path, and the maximum amount that would be deductible if you give it away, and give that amount to your donor advised fund (DAF) (see Donor Advised Funds) and take the charitable deduction. You and others you designate grant funds from the DAF just to our church or to church and other charities over time, during life and at and after end of life.

.png)

Simply put, each year the government gives you money back, in the form of tax savings, merely for transferring money from your right hand, your personal estate, to your left, your DAF. Both the tax savings added back to the estate and the amounts given to the DAF grow for eventual giving (DAF amounts growing faster because tax-free).

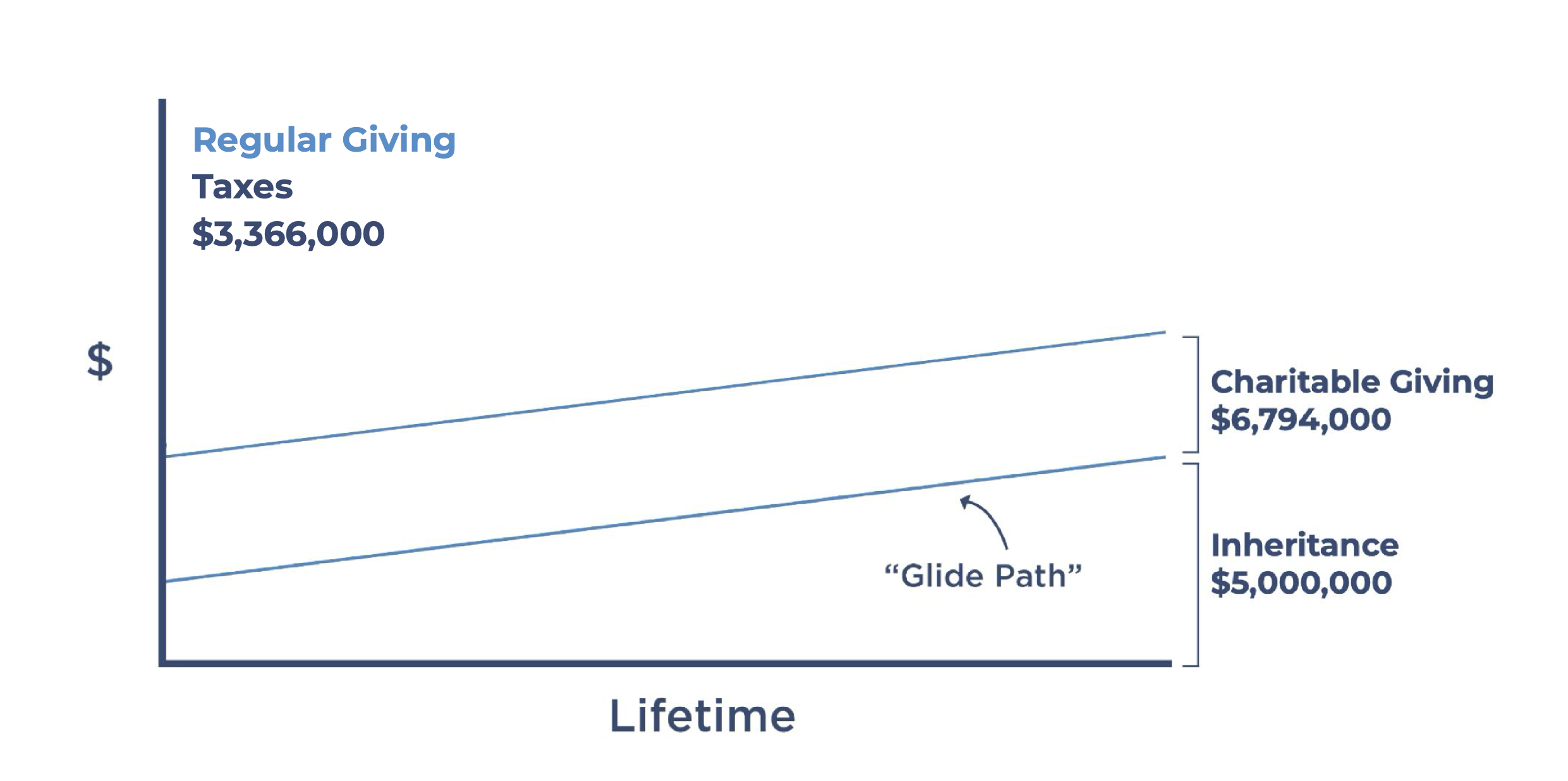

Here’s an example: Joseph and Myrna Banks are 52 years old. Joseph currently earns a high salary as CFO of a manufacturing company. The Banks have four children and a beginning estate of $3,500,000. They earn annual taxable compensation of $400,000, and they tithe 15% of their total realized income each year, or $59,000. Their annual personal expenditure is $180,000. The true wisdom and love of Christ in their hearts prompts the Banks to plan to leave an estate to their children of $5,000,000 and bequeath the rest of their estate to church and charity.

Here are possible results – presented in two different ways – at end of the Banks’ joint life expectancy when they merely continue their regular giving, assuming certain additional financial circumstances:

GIVING EXAMPLE — ACCELERATED GIVING – THE BANKS GIVE AT END OF LIFE

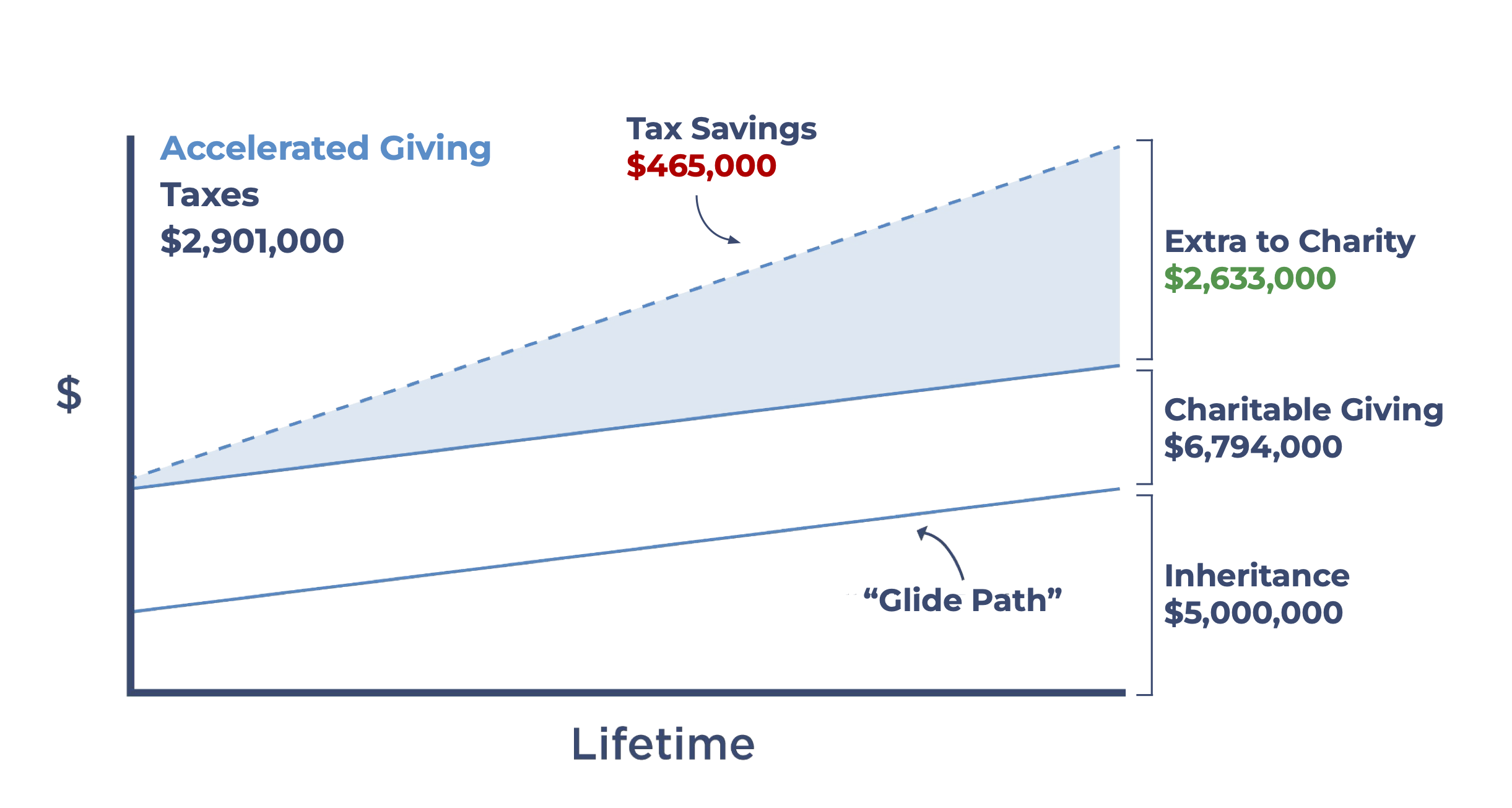

And here are possible results at the end of joint life expectancy under the same financial assumptions of instead accelerating giving to remaining years of high taxable income:

GIVING EXAMPLE — ACCELERATED GIVING – THE BANKS GIVE DURING TAXABLE INCOME YEARS

Personal Expenditure remains the same; ending estate (inheritance) remains the same; but lifetime taxes go down significantly but not by a startling amount, $465,000; while total giving, during life and from the estate and the DAF, goes up by more than $2,600,000. The effect is truly remarkable even when these givers give accelerated extra amounts over only five years. With higher levels of excess taxable income relative to amounts intended for heirs, the amount of giving can more than double.

By starting today, you can radically increase the wealth you give over and after your lifetime even when making very conservative projections and proceeding very cautiously. It just takes a little planning with the help of your financial advisor and the PCA Foundation.

Real Estate Gifts with Reserved Life Estates

One of the largest assets that most people will ever own is their home. For others, it is a farm or ranch. Such people may desire to give home or farm to church or other charity ultimately, but cannot do so until end of life because they must continue to live in the home or earn income from the farm. But bequeathing the property (Charitable Bequests) fails to produce a charitable deduction and the corresponding tax savings (tax subsidy) that enables greater giving.

In a gift of residence, farm, or ranch with a retained life estate (RLE), you donate the property to your donor advised fund (DAF) at the Foundation (see Donor Advised Funds) while retaining the right to live on or use and earn income from the property for your lifetime. At the end of life, the Foundation sells the property and places the proceeds in your (DAF), from which it makes grants just to our church or to church and multiple other charities immediately or over time, pursuant to instructions from you or from successor advisors you have designated.

Like a charitable remainder trust (Charitable Remainder Trusts) or charitable gift annuity (Charitable Gift Annuities), an RLE is a gift that effectively gives back to you. You receive an immediate charitable deduction for the present value of the projected value of the real estate at the end of your life. This is a deduction and tax subsidy for greater giving that you would not receive at all if you merely bequeath the real estate to church or charity in your will. Meanwhile, you may continue to live in and use the property, effectively (or even actually) earning income from it.