Donor Advised Funds and Other Giving Tools

Reduce Your Taxes. Simplify Your Giving. Advance God’s Kingdom.

Click on an item below for specific instructions on how to make a gift to your fund at the PCA Foundation, Inc.

Our church and the PCA Foundation provide general information and gift ideas for consideration by you and discussion with your own legal and other professional counsel, and not legal or other professional advice for your reliance. Neither our church, the PCA Foundation, nor any employee or other agent of either is permitted to or will provide legal or other professional advice or representation, and we urge you to seek legal and other professional counsel before making any significant gift.

Why Use Giving Tools

Let’s consider first why you would use giving tools – or employ any other tax-efficient giving strategy.

It’s not to make yourself wealthier post-gift because no charitable giving can ever leave the giver with greater wealth, no matter how much tax it saves. Nor is it to give wealth to charity instead of the government because tax savings can only ever be a percentage less than 100 of the amount given. To illustrate simply, the giver with a marginal tax rate of 35% who gives $1,000 to charity and deducts $1,000 from his taxable income effectively saves only $350 in tax. So, after the gift, and after the tax rebate, he still is $650 poorer than before he made the gift.

No, the reason to make the gift that saves the most in taxes is to be able to give MORE. In our simple example, the $350 tax savings produced by the charitable deduction mean that the $1,000 gift effectively cost our giver only $650. As every amateur economist knows, when something costs less, one can buy more of it. Here, the giver can give more – at least $350 more. Calculated more precisely, the giver can give the amount of wealth with which he is willing to part, $1,000, divided by 1 minus the tax rate, 65%: he can give $1,538 ($1,000/.65), or $538 more.

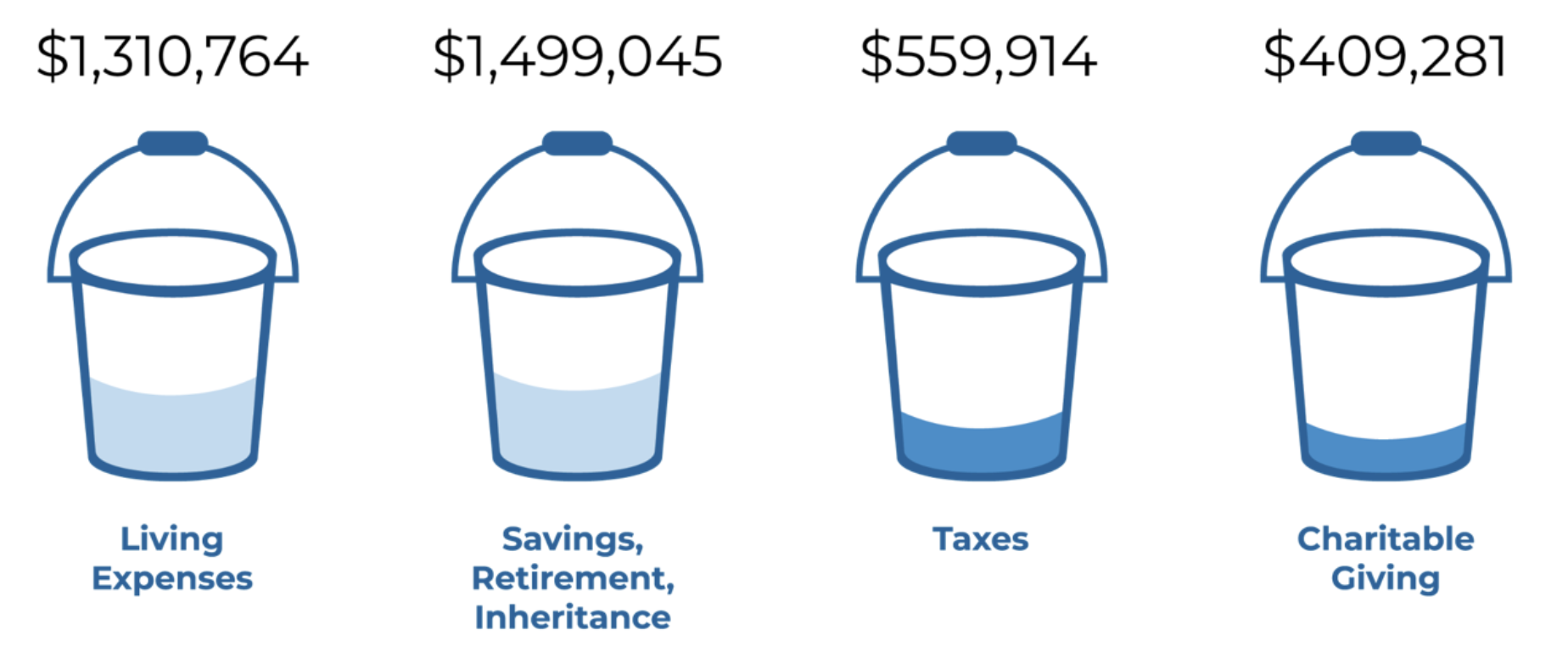

Or envision four “buckets” into which you can place your income and wealth:

Whenever you decide how much to place in the giving bucket as cash, you actually are deciding in your Spirit-changed heart how much to keep in the consumption and savings buckets. You then employ non-cash giving to move greater tax savings from the tax bucket to the giving bucket, while leaving the same amounts in the consumption and savings buckets.

In a word, use giving tools such as donor-advised funds and you can give more to our church and other charities.

Donor Advised Funds

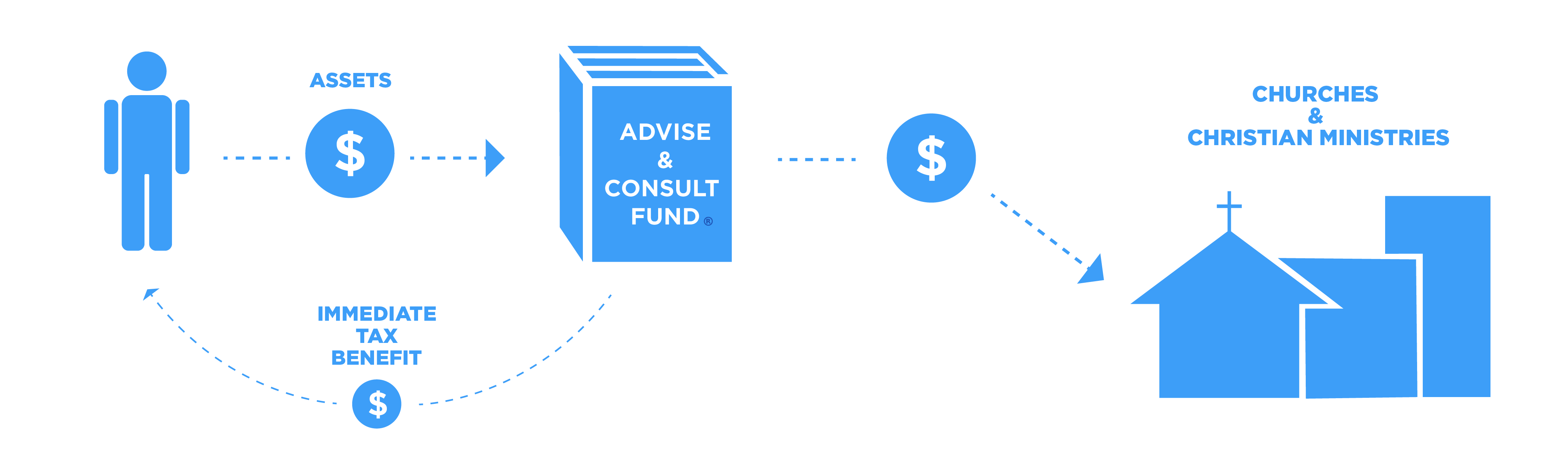

A donor advised fund (DAF) enables you to give in one year, and take a charitable-contribution deduction to reduce taxable income that year, and then advise grants of varying amounts to our church or our church and multiple other charities in future years. Deduct now. Give (ultimately) later. You can give to a DAF not only cash, but also stocks, bonds, mutual funds, real estate, or shares of a privately-held business, or other appreciated non-cash assets (see Non-Cash Gifts).

But why not instead give the entire amount you desire to give to an end-user charity in the current year? There could be one or more of several reasons, including anonymity, one charitable contribution receipt, and ease of giving. However, the most common reason not to give all to one or more end-user charities all in the current year is that the portion of income the donor sets aside in his heart for Kingdom giving is so large that he does not want, or does not think it wise, to give it all to one charity all in one year.

But if you don’t want to give all to end-user charities in the current year, why not wait and give the amount you desire to give from current-year extraordinary income to the multiple end-user charities over a number of future years, and take the charitable-contribution deduction in those years? The most thoughtful reason for not following that approach, but instead giving to a DAF in the current year, is to maximize the tax savings by giving and deducting against the large taxable income, and thereby be able to give more, as a result of the following dynamics:

First, tax savings realized in one year are more valuable than tax savings realized in future years. (This is the time value of money.)

Second, funds placed in a donor-advised fund earn more because they earn tax-free.

Third, a DAF facilitates giving for the benefit of multiple charities a single high-value non-cash asset pre-sale rather than cash proceeds after sale, and such giving greatly maximizes the effective tax deduction, tax savings, and giving.

Fourth, and most significantly, due to the limitation on the charitable deduction to 30% to 60% of adjusted gross income (AGI), the full amount you want to give from current-year extraordinary income may not be deductible if given over future years, or retirement years, when AGI returns to normal, substantially lower levels.

Here’s an example: the Hudsons are a couple with regular annual compensation and other ordinary taxable income of $150,000, and investment and retirement accounts of $1,000,000. They typically expend each year $105,000, and want to tithe $15,000. But in the current year and the next their taxable income will jump by an extra $500,000 each year, of which the love of Christ and expected charitable need compel them to set aside 30%, or $300,000, which they intend to give to our church five years from now, when they will retire and when they expect the church to launch a capital campaign. The Hudsons also expect that after next year their income will return to normal levels, and when they retire in five years will drop effectively to zero.

Here are possible results at the end of ten years (the number of years to retirement and gift, plus five years for carrying forward deductions exceeding the AGI limitations) if the Hudsons do not give in the years of extraordinary income but set aside the desired amount within their personal accounts to give in the fifth year, assuming certain additional financial circumstances:

DAFS – THE HUDSONS SET ASIDE CHARITABLE GIFT IN PERSONAL ACCOUNTS

And here are possible results at ten years assuming the same financial circumstances if the Hudsons instead give the desired amount to their DAF in the years of extraordinary income:

DAFS – THE HUDSONS GIVE CHARITABLE AMOUNT IMMEDIATELY TO DAF

Personal Expenditure remains the same; ending savings remain the same; but taxes go down significantly, by $202,000 to an amount of $358,000. How? The Hudsons fully utilize the otherwise partially wasted deduction, and remove the amount set aside for giving from the taxable personal estate to the non-taxable DAF. And total giving goes up significantly, to a total of $667,000, because the Hudsons are able to give those tax savings and the tax-free earnings on amounts given to the DAF. Put another way, every dollar the Hudsons give to the DAF costs them less, so they are able to give away more dollars. The Hudsons can give $258,000 more if they give to a DAF in the years of extraordinary income rather than merely setting aside amounts for future giving within their personal estate.

A variation on this theme of timing your giving by using a DAF in order to maximize the tax savings for greater giving is a technique called “bunching.” As many will know, when you itemize your deductions you cannot also take the currently generous standard deduction ($32,200 for married couples filing jointly in 2026. Bunching allows you to realize the tax savings of both the standard deduction and giving deduction. Here’s how: you give to your DAF in the current year the amount you anticipate giving in the current year and the next year or two, and deduct that amount as an itemized deduction in the current year. For the next one or two years you do the giving you had planned not from your income but as grants from your DAF, and you take the standard deduction. You effectively achieve a double deduction and double tax savings for the second or second and third years.

Open an Advise and Consult Fund with the PCA Foundation

Open an Increase Fund with the PCA Foundation

IRA Charitable Rollovers

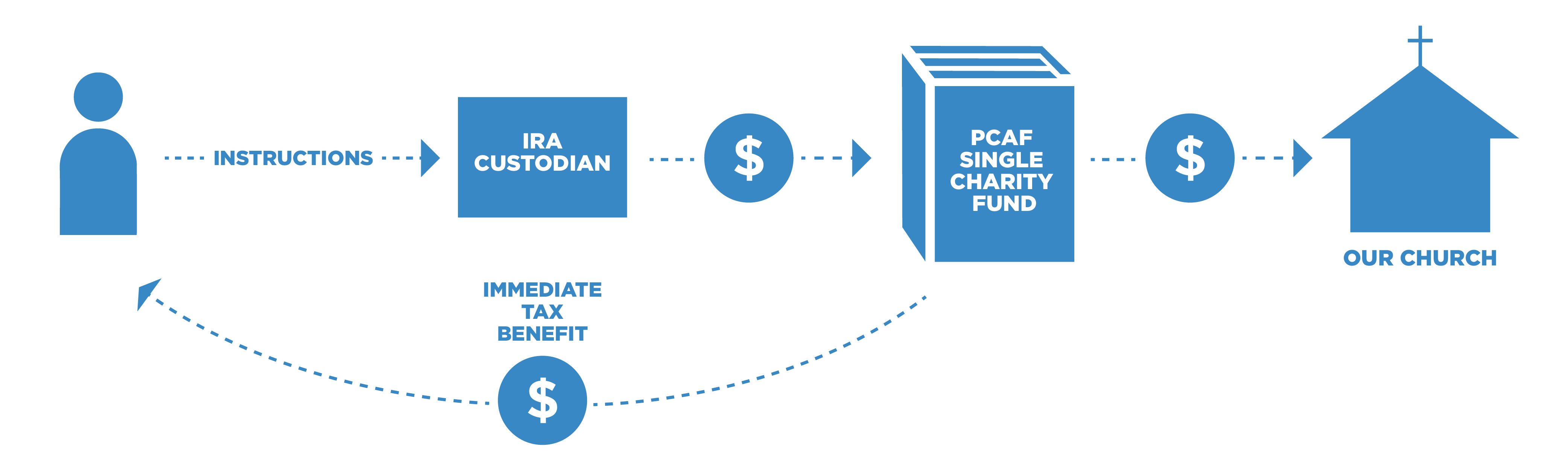

A qualified charitable distribution (QCD), also called an IRA charitable rollover, is a direct rollover from an individual retirement account that you make when you are age 70 ½ or older. (Note that you effectively can direct a QCD from a 401(k) account by first rolling over the amount from the 401(k) into an IRA.) The maximum amount you can roll over as QCDs in 2026 is $111,000.

The amount of your QCD counts against your required minimum distribution from your IRA, and is excluded from your taxable gross income. Such an exclusion is the equivalent of a deduction for a cash charitable contribution. But the QCD comes with an added tax-saving benefit: it allows you also to take the standard deduction (which you could not take if you had taken the itemized deduction for a cash charitable contribution). This combination of exclusion and standard deduction is effectively a double deduction that saves taxes for greater giving. The exclusion achieved by a QCD also may reduce taxes on Social Security payments, and lower Medicare premiums, thereby facilitating even more giving.

You may not direct a QCD to a donor advised fund, but may direct it to a single charity fund at the PCA Foundation and make grants from that fund over a number of years only to that charity. If you intend to distribute all of a QCD to our church in one year, simply instruct your IRA custodian to send the QCD directly to us. If instead you want to distribute a substantial QCD to our church or another charity over two or more years, follow the instructions for initiating a charitable rollover to the PCA Foundation.