Income and Wealth Reservation Gifts

Giving Solutions That Return Income to Increase Giving

Click on an item below for specific instructions on how to make a gift to your fund at the PCA Foundation, Inc.

Our church and the PCA Foundation provide general information and gift ideas for consideration by you and discussion with your own legal and other professional counsel, and not legal or other professional advice for your reliance. Neither our church, the PCA Foundation, nor any employee or other agent of either is permitted to or will provide legal or other professional advice or representation, and we urge you to seek legal and other professional counsel before making any significant gift.

Why Split-Interest Gifts

Let’s consider first why you would want to give to charitable trusts or in exchange for annuities that return income or principal to you. The first answer is either (i) you want to receive a deduction now for an eventual gift in order to save income taxes or save them sooner, or, less commonly, (ii) you want to reduce the value of a gift to your children or other heirs by giving to charity now in order to save gift and estate taxes. But why would you want to save income or estate taxes by giving in a split-interest arrangement – or employing any other tax-efficient giving strategy?

It’s not to make you or your beneficiaries wealthier post-gift because no charitable giving can ever leave the giver or his beneficiaries with greater wealth, no matter how much tax it saves, and because the income or wealth returned in a split-interest arrangement is the same income one can achieve or wealth one can retain by keeping rather than giving. Nor is it to give wealth to charity instead of the government because tax savings can only ever be a percentage less than 100 of the amount given, and in a split-interest arrangement, a percentage far less than 100. To illustrate simply, a 55-year-old giver with a marginal tax rate of 25% who gives $100,000 to a charitable remainder unitrust that pays him income of 5% each year for life and pays charity the remainder, is able to deduct $31,450 from his taxable income. He effectively gives away that $31,450, keeps $68,550, and saves $7,863 in tax. So, after the gift, and after the tax rebate, he still is $23,587 poorer than before he made the gift ($31,450 gift minus $7,863 tax rebate).

No, the reason to make the gift that saves the most in taxes given the giver’s need for income or retained wealth is to be able to give MORE. In our simple example, the $7,863 tax savings produced by the charitable deduction mean that the $31,450 gift effectively cost our giver only $23,587. As every amateur economist knows, when something costs less, one can buy more of it. Here, the giver can give more – at least $7,863 more.

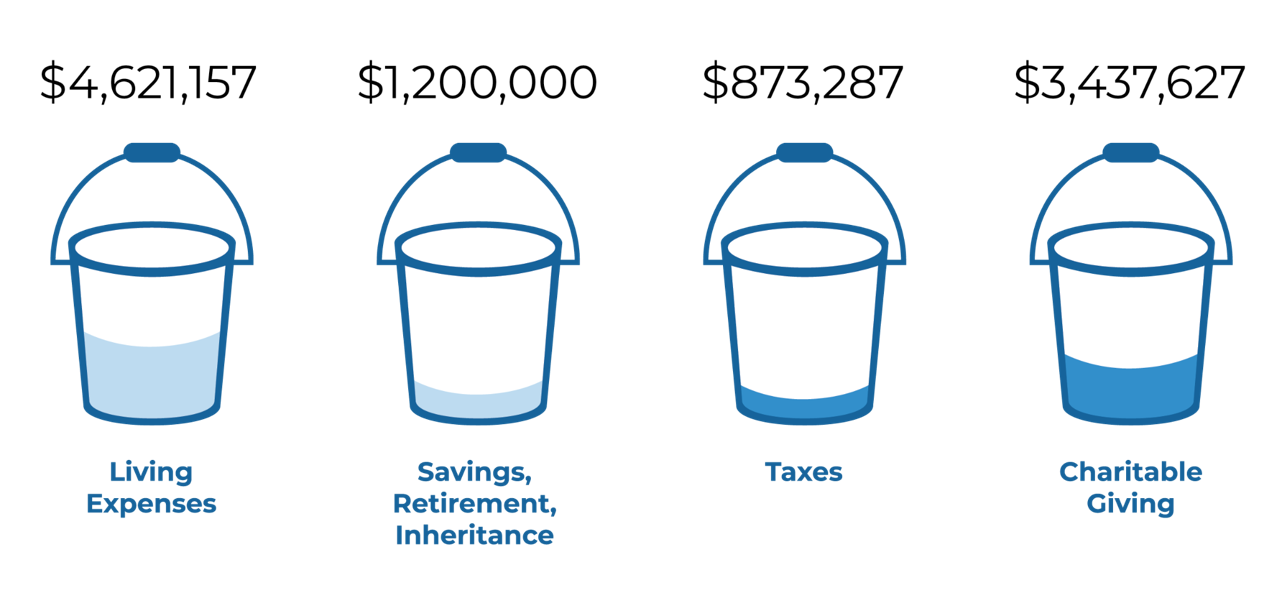

Or envision four “buckets” into which you can place your income and wealth:

Whenever you decide how much to place in the giving bucket as cash, you actually are deciding in your Spirit-changed heart how much you must keep in the consumption (or income) and the inheritance buckets. You then give in a split-interest arrangement in order to move greater income or estate tax savings from the tax bucket to the giving bucket, while leaving the same amounts in the income and inheritance buckets.

In a word, give in a split-interest arrangement and you can effectively give more to our church and other charities while receiving the income you or your beneficiaries need and bequeathing the same to your children and other heirs.

Charitable Remainder Trusts

Givers achieve the greatest tax savings for greater giving by giving an appreciated asset or other wealth outright during life rather than at death (see Accelerated Giving), but many cannot give outright now. They instead must wait for years or even until end of life to give because they or their heirs need to live on the income thrown off by the asset or wealth for the remainder of life or for a term of years. The delayed deduction reduces or eliminates the tax savings for greater giving.

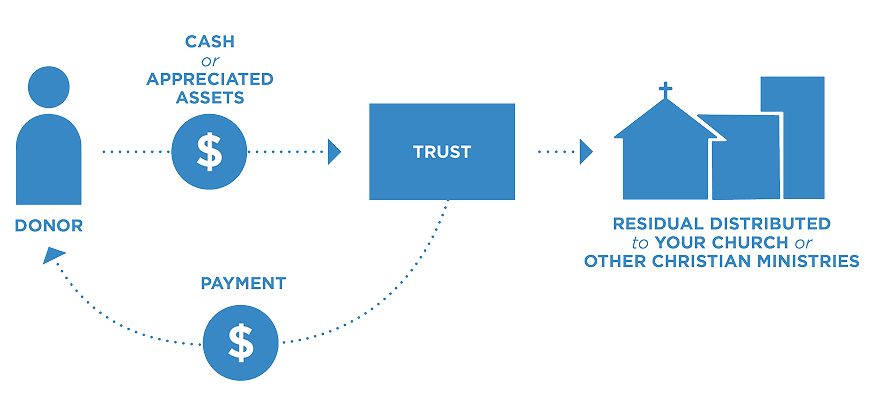

A Charitable Remainder Trust (CRT) solves this problem. When you give to a CRT it pays you or beneficiaries you name an income stream for life or lives or for a period of years up to 20, and pays the remainder to our church or to your donor-advised fund (see Donor Advised Funds) for ultimate distribution just to our church or to church and multiple other charities.

You take a charitable tax deduction now even though you or your heirs continue to receive income on the gift amount. This immediate deduction effectively reduces income tax more than a later deduction. In fact, if the CRT pays the remainder to charity at the end of your life, you are deducting now an amount that you otherwise would never deduct, achieving tax savings for greater giving that you would never achieve. Moreover, a remainder payment paid to charity will be larger than a bequest to charity at death because it will grow in the trust, unlike in your personal estate, partially tax-deferred and partially tax-free.

For additional tax savings for greater giving, you may fund a CRT with all or part of an appreciated non-cash asset you desire to sell in order to capture the gain and increase and diversify your or your beneficiaries’ income streams. The CRT sells the funding asset free of capital gains tax, and that capital gains tax is paid only when, if ever, it is paid out to you or your beneficiaries. All this results in a higher – and diversified – principal that produces higher after-tax income payments to you or your beneficiaries that enable you to give more while providing the intended income to you or your beneficiaries.

Two important considerations about CRT funding assets: first, you must give the asset to the CRT before entering into a binding agreement to sell. Second, you cannot fund a CRT with significantly debt-encumbered assets or with S corporation stock.

Here’s an example: the Smiths are a 65 year-old couple with two adult children. They have a typical investment portfolio of $750,000, but also own commercial real estate valued at $3,000,000 with a basis of $300,000. The love of Christ spread through the Smiths’ hearts by the Holy Spirit compels them to give eventually at least twenty percent of the real estate gain, or $540,000 to our church and a mission agency, to leave $600,000 to each of their children, and to leave whatever is the remainder to our church and a few other charities. However, the Smiths anticipate that they will need at least part of the income earned each year on their current estate, including the real estate, to pay their anticipated living expenses over their lives.

Here are possible results at end of the Smiths’ joint life expectancy when they sell the real estate, place the proceeds in the estate, and give from and live off the income earned within the estate, assuming certain additional financial circumstances:

GIVING EXAMPLE: CHARITABLE REMAINDER TRUST – THE SMITHS GIVE AT END OF LIFE

And here are possible results at end of life expectancy under the same financial circumstances if the Smiths instead give to a CRT that pays them the income they require for their anticipated living expenses:

GIVING EXAMPLE: CHARITABLE REMAINDER TRUST – THE SMITHS GIVE NOW TO CRUT

By giving to the CRT, the Smiths are able to cover the same amount of personal expenditure, and to leave the same inheritance to their children. But they reduce their income tax significantly, by $465,000, due to the deferral of tax on the capital gain, and the immediate charitable deduction; and they increase their charitable giving even more due to those tax savings and earnings on them within the estate, deferral of tax on a portion of earnings within the CRT, and outright avoidance of tax on another portion of those earnings. The Smiths can give $971,000 more to their church and other favorite charities while continuing to live off the earnings of their current wealth.

CRTs are flexible and can be tailored to your specific giving and income goals. You may create one during your lifetime or through your will. Additionally, you may make contributions to a CRT over several years for any number of reasons, including spreading out contributions to assure that they are fully deductible under adjusted-gross-income limitations (see Donor Advised Funds). Variations of a CRT include:

Net Income Charitable Remainder Unitrust (NICRUT), which pays to the income beneficiaries each year the lesser of the prescribed payout percentage and the net income of the CRT, in the event the CRT is funded with a hard-to-sell non-cash asset.

Net Income with Makeup Charitable Remainder Trust (NIMCRUT), which pays the lesser of the payout percentage and the net income each year, but pays additional amounts in future years when net income increases to recover the amounts of payout percentages not paid in prior years due to the net income limitation.

Flip Charitable Remainder Unitrust (flip-CRUT), which initially pays the lesser of the payout percentage or payout percentage plus makeup amount, and net income, but upon the occurrence of a particular event begins paying the payout percentage regardless of net income. The flip-CRUT may be used when funded with a hard-to-sell asset, or when you want to build up the value of the CRT tax-free without starting payments and paying income tax on them until some life event such as retirement.

Download the PCA Foundation’s informative guide to learn more about the advantages of a Charitable Remainder Trust.

CRTs operate as a practical matter much like Charitable Gift Annuities (CGA) (see Charitable Gift Annuities). However, a CRT is much more flexible than a CGA, and opens the possibility of income payments to you or your beneficiaries increasing as the CRT’s investments appreciate over time. On the other hand, a CGA is a simpler giving tool than a CRT, is less costly to establish and administer, and makes payments guaranteed by the Foundation and backed by its assets.

Charitable Gift Annuities

Givers achieve the greatest tax savings for greater giving by giving an appreciated asset or other wealth outright during life rather than at death (see Accelerated Giving), but many cannot give outright now. They instead must wait until end of life to give because they need to live on the income thrown off by the asset or wealth for the remainder of life or for a term of years. The delayed deduction eliminates the tax savings for greater giving.

Other givers are not interested primarily in giving but in a steady income stream, and so intend to purchase an annuity, but are happy to support their church or other charity by purchasing the annuity from it.

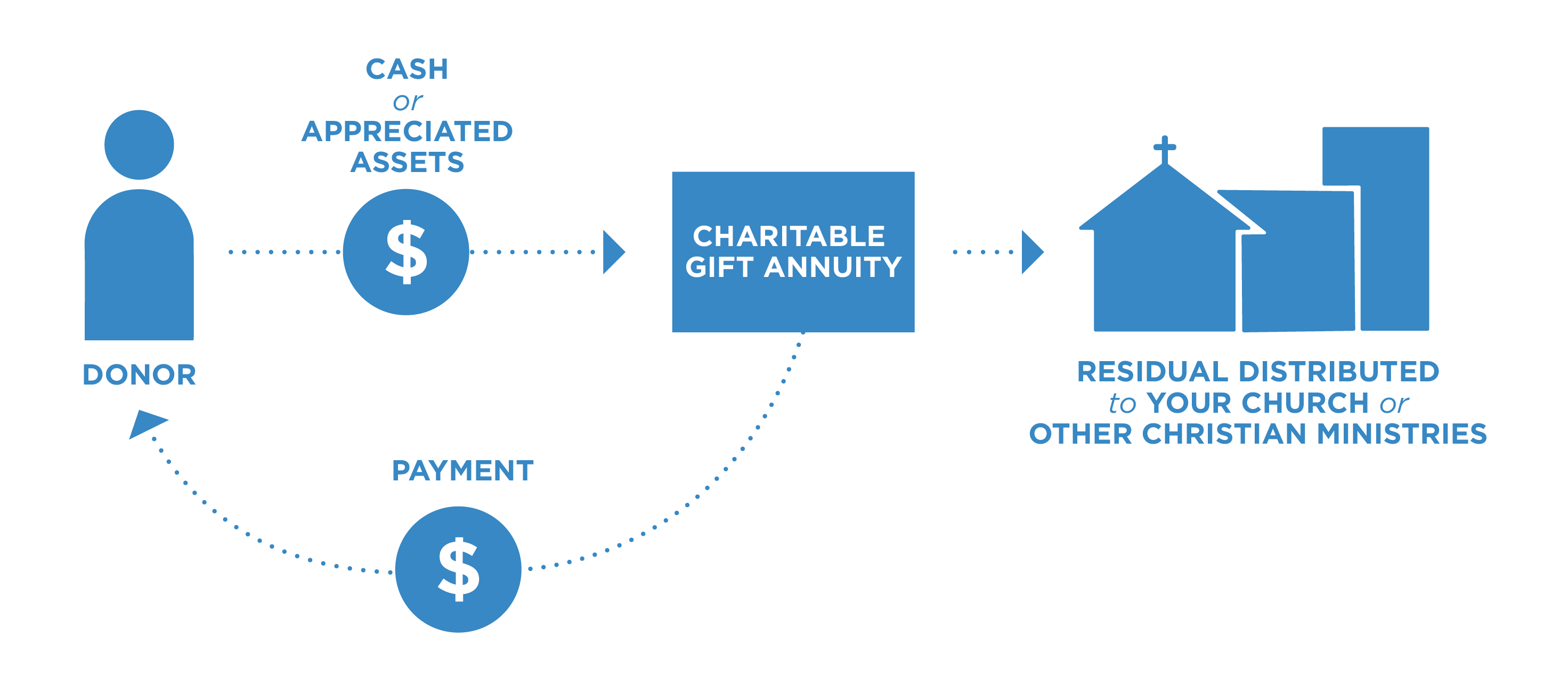

Giving in exchange for a Charitable Gift Annuity (CGA) – part gift and part annuity purchase – accomplishes these objectives. When you purchase a CGA from the PCA Foundation, the Foundation pays you, you and your spouse, or another person or two you designate, an income stream for life or lives, and pays what remains of your invested initial payment to your donor-advised fund (see Donor Advised Funds) for ultimate distribution just to our church or to our church and multiple other charities. (The Foundation is at times able to reinsure the annuity with a commercial annuity provider, thereby enabling immediate payment of the projected charitable portion of your initial payment to your donor-advised fund.)

You take a charitable tax deduction now even though you or your designees are receiving annuity payments – effectively income on the gift amount. This is a deduction for the present value of a gift to charity at end of life, which you would not be able to take at all if instead you actually gave to charity at end of life as a charitable bequest. This deduction produces tax savings for greater giving. Moreover, the amount remaining for charity when annuity payments cease will be larger than a bequest to charity because the amount you initially pay for the CGA will grow in the Foundation tax-free.

For additional tax savings for greater giving, you may fund a CGA that pays an annuity to you or to you and your spouse with all or part of an appreciated non-cash asset you desire to sell in order to capture the gain and increase and diversify your income streams. (You may not effectively fund a CGA that pays persons other than you or your spouse with such an asset.) You defer over your life expectancy capital gains tax on the portion of the asset with which you purchased the annuity, greatly decreasing the effective amount of that tax. Meanwhile the Foundation sells the asset free of capital gains tax (or subject to only one-half of the capital gains tax only on the portion of the asset with which you did NOT purchase the annuity, if the asset is S Corporation stock.) (See S Corporation Gifts). All this results in tax savings that substantially increase how much you can give to our church and other charities you desire to support. As with all non-cash gifts, it is important to remember that you must purchase the CGA with the asset before you enter into a binding contract to sell it (otherwise, the IRS will treat your purchase of the CGA followed by sale of the funding asset as a taxable sale of the asset followed by a purchase of the CGA, eliminating the tax savings just described).

Variations of the standard CGA include the deferred gift annuity, which begins making annuity payments in a future year. You give for the annuity and take an immediate deduction, but do not begin receiving annuity payments, and paying tax on them, until you project you will need them. If you are not sure you ever will need the annuity payments, you may choose a flexible deferred gift annuity, which begins making annuity payments only when you decide to begin taking them. The amount of the annuity payments increase for each year they are deferred.

CGAs operate as a practical matter much like Charitable Remainder Trusts (CRT) (see Charitable Remainder Trusts). However, a CGA is a simpler giving tool than a CRT, is less costly to establish and administer, and makes payments guaranteed by the charity and backed by its assets. On the other hand, a CRT is much more flexible than a CGA, and opens the possibility of income payments to you or your beneficiaries increasing as the CRT’s investments appreciate over time.

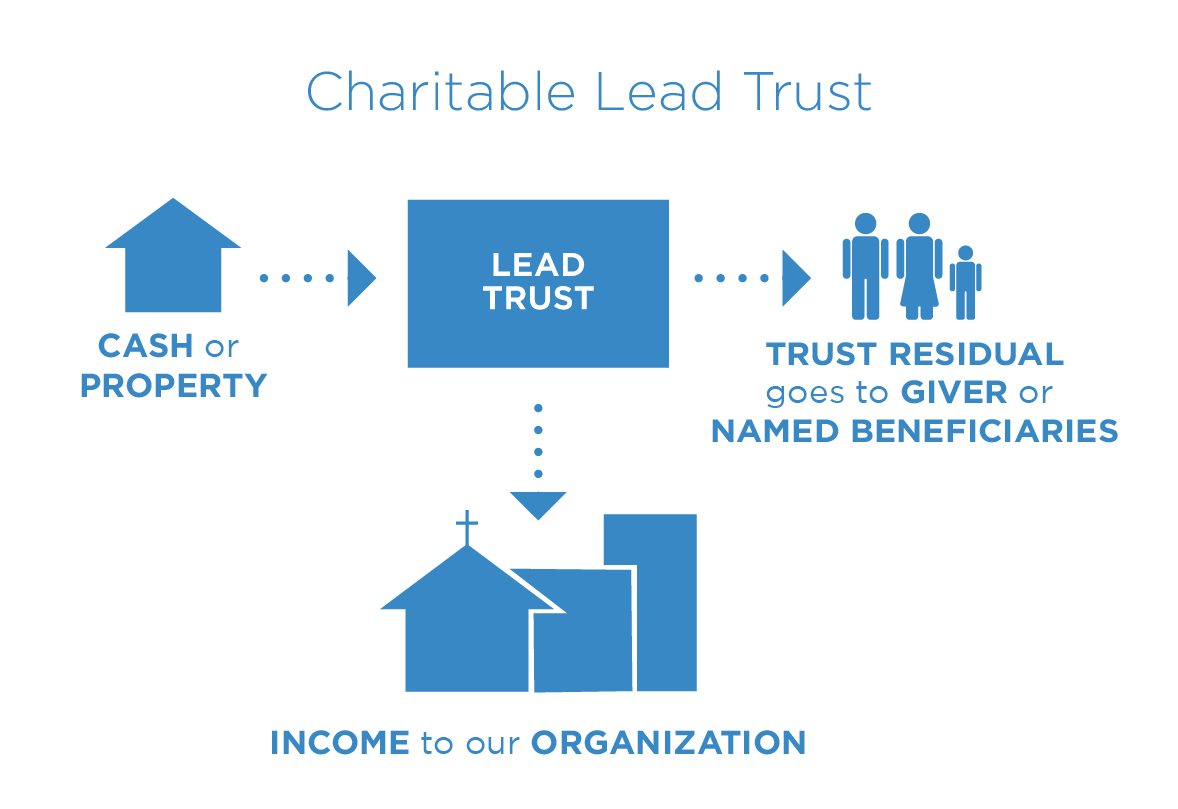

Charitable Lead Trusts

A Charitable Lead Trust (CLT) operates in reverse of how a Charitable Remainder Trust (CRT) operates (see Charitable Remainder Trusts). The CLT first pays an income stream to charity – to our church or to your donor advised funds from which you can make grants just to our church or to our church and multiple other charities (see Donor Advised Funds) – every year of a measuring life or for a set number of years. After that period of charitable distribution, the assets remaining in the CLT go back to you or to beneficiaries you name. The measuring life expectancy must be the life of you or your spouse, or any ancestor of the remainder beneficiaries or the ancestor’s spouse.

A CLT that distributes the remainder back to you is a Grantor CLT. A CLT that distributes the remainder to your heirs or other beneficiaries you designate is a Non-Grantor CLT. Both kinds of CLTs are taxable entities (and in this respect differ from tax-exempt CRTs). Like taxable individuals, CLTs can deduct the charitable distributions they make, but better than individuals, can deduct those charitable distributions up to 100% of the CLT’s income. The major difference between a Grantor CLT and a Non-Grantor CLT is that most Grantor CLTs are treated as part of your estate – really, as you – and you pay income tax on the CLT’s income, while a Non-Grantor CLT is treated as an entity separate from you, and its assets as outside your estate, and it pays the income tax on its income. These rules mean that you use a Grantor CLT to accomplish different tax savings than the tax savings you use a Non-Grantor CLT to accomplish.

When you give to a Grantor CLT, you immediately deduct the present value of the projected distributions the CLT will make to charity in future years, reducing your income taxes now; but then you recognize as your own taxable income the trust’s income in those years. If your income in the current year is significantly higher than in the future years of the trust, and therefore taxed at higher marginal tax rates, you greatly reduce the total income tax you pay, thereby enabling greater giving.

You also can use a Non-Grantor CLT to save income taxes for greater giving when you already are giving amounts of income that exceed the adjusted-gross-income deduction limitations (see Donor Advised Funds). If in a year you already have given an amount that is 50% or more of your income, and you want to give in addition all the income produced by a particular asset or particular assets you own, you will not be able to fully deduct that additional giving. This means you effectively will pay income tax on part or all of the additional income you give away, reducing how much you can give. However, if you give the income-producing assets to a Non-Grantor CLT, the CLT will be able to deduct its distributions to charity up to 100% of the income it realizes from those assets, allowing you effectively to give through the CLT all that income without reduction for income taxes.

But the primary use of a Non-Grantor CLT is not to save income taxes, but to save the exorbitant 40% estate and gift tax. A Non-Grantor CLT can be useful to you in this way only if your estate at death is likely to exceed the estate-and-gift-tax exclusion amount, which effectively is $30 million for a married couple in 2026. If you project an estate at death above that amount, read on.

When you give to a Non-Grantor CLT, you are deemed to make a gift to your heirs or other beneficiaries you name equal to the present value of the remainder amount they are projected to receive. That gift is subject to the estate and gift tax, but gift, along with tax, is reduced by the present value of the projected annual income distributions to charity. But those tax savings come at the cost of reducing the inheritance, and are not the point of a Non-Grantor CLT. The point instead is that the present value of the projected annual income distributions to charity is calculated assuming the government-published interest rate at the time of the gift. When the CLT grows faster than that rate, as CLTs frequently do for a variety of reasons, the remainder actually distributed to your beneficiaries is larger than the projected remainder on which the estate and gift tax was charged. You effectively have reduced tax on the inheritance you leave to your heirs. These effective tax savings enable you to give more while your heirs keep the same.